Financial inclusion ensures equal access to financial services so women can mobilise their savings, obtain credit and make financial decisions independently.

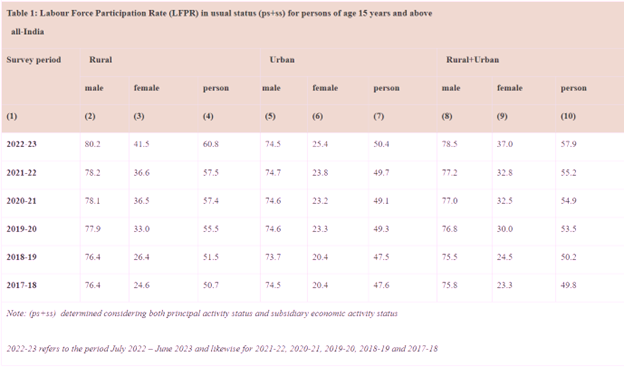

Women comprise nearly half the population in India, but their economic participation is only 37 per cent, according to the Periodic Labour Force Survey report (2022-23).

Their participation in economic activities leads to equitable distribution of wealth and aids the achievement of the Sustainable Development Goals. But despite the efforts to promote financial inclusion, disparities persist

Women continue to face inequality socially, politically and financially. For achieving gender equality, financial empowerment of women is crucial. Their inclusion in the financial system can significantly address this imbalance.

Financial inclusion is also a critical aspect of the International Women’s Day 2024 theme “Invest in women”.

That’s where self-help groups come in. Self-help groups play an important role in digital financial literacy, enabling digital financial inclusion and eventually empowering women.

Financial inclusion ensures equal access to financial services so women can mobilise their savings, obtain credit and make financial decisions independently.

During last year’s G20 deliberations, financial inclusion emerged as a fundamental driver of economic growth.

Women often face challenges accessing banking services due to distance, cultural barriers, and restrictive social norms. These constraints include limited mobility to access bank branches and the absence of female-friendly banking infrastructure.

The major policy to achieve financial inclusion undertaken by the government of India was Pradhan Mantri Jan Dhan Yojna, which was introduced in 2014 to provide financial services to people who either have no access or limited access to banking services.

Under the programme, 500 million people have benefited by their inclusion in the formal banking system, out of which women open 55 per cent of bank accounts. They digitised the banking system by providing people-centric benefits. This included direct benefit transfers (DBTs) that contribute to inclusive growth, especially for the underprivileged — notably women — and offer convenient and accessible banking options.

The Jan Dhan, Adhar and Mobile (JAM) scheme has enabled mobile banking, digital wallets and online transactions, which have the potential to bridge the gender gap in accessing financial services.

A significant increase in digital financial transactions during COVID-19 offered a new area of transformation towards how people do banking. Under the Digital India programme, Pradhan Mantri Gramin Digital Saksharta Abhiyan (PMGDISHA) aims to bridge the digital divide by targeting rural populations, particularly women and girls, with over 53 per cent of women benefiting.

Digitalisation has revolutionised the financial system by including more of the population in this domain. However, challenges persist in adopting digital financial services, including the digital divide, cyber security, data privacy and lack of financial literacy.

Adoption of digital technologies requires digital financial literacy regarding the use of mobile phones and the internet. But women in India either do not own these resources or do not know their usage, which poses a constraint in the adoption of digital financial inclusion.

A Global System for Mobile Communications (2020) report shows that a woman is 26 per cent less likely to own a mobile phone and 56 per cent less likely to use mobile internet than a man in India.

According to the National Family Health Survey (2019-21), only 33 per cent of women in India have used the internet compared to men, who comprise 57 per cent of the total population.

In rural India, there is a significant gender disparity in internet usage, with men being twice as likely as women to have accessed the internet (49 per cent versus 25 per cent).

(PC: @MoRD_GoI/X)

In India, self-help groups (SHGs) have aided the financial inclusion of women through the SHG-Bank Linkage Programme. The Bank Sakhi programme by the National Rural Livelihoods Mission trains self-help group members to work as banking correspondents in rural districts. The programme has improved women’s exposure to financial services, driving up digital transactions in rural India.

For instance, Rajasthan’s State Rural Livelihood Mission (SLRM) has initiated mobile wallet M-Pesa in collaboration with Vodafone for instant payments, money transfer, and utility payments. Eight hundred SHGs and 9000 SHG members use their M-Pesa wallet to deposit their loan repayments into the SHG account.

Self-help groups are active participants in various government schemes and programmes. They are growing at 10.8 per cent annually, with 5.7 per cent annual growth in credit disbursement. The government aims to have 0.125 million trained banking correspondents nationwide by 2023-24.

These banking correspondents-sakhis are members within the self-help groups who perform banking functions by handling deposits, credit, micro-insurance, mutual funds and promoting savings on their behalf. They also penetrate rural areas by offering digital services, including e-commerce and online education, that benefit the community and help them secure sustainable livelihoods.

Women prefer non-institutional loans and credit from self-help groups where the credit source is not maintained. Hence, self-help groups become an important source of credit for women.

As India continues its journey toward comprehensive financial inclusion, combining educational initiatives, gender-sensitive approaches, and digital interventions will be critical.

Self-help groups play a crucial role in increasing access and fostering active participation by leveraging the utilisation of resources through government channels. By doing so, India advances financial inclusion as a powerful tool for economic empowerment and societal well-being.

There is a need for sustained efforts and targeted interventions to create a more inclusive and equitable financial landscape.

To bridge the gender gap in access to digital financial services, strategies could include promoting financial literacy for women, encouraging low-cost digital services, and penetration of direct benefit transfers, particularly for elderly women who find it difficult to access government schemes and funds due to limited physical mobility.

Financial literacy programmes and technology-driven solutions are essential to create an inclusive financial ecosystem.

The research was undertaken with financial assistance from the Indian Council for Social Science Research (ICSSR).

The authors are all from Manav Rachna International Institute of Research and Studies, Haryana, India. Durairaj Kumarasamy is Associate Professor and Head, Department of Economics, School of Behavioural and Social Science; Sukhvinder Kaur is a Research Scholar in the Department of Economics, School of Behavioural and Social Science; Vandana Jain is a Research Assistant in the School of Media and Humanities and a Research Scholar in the Department of Economics, School of Behavioural and Social Science.

Originally published under Creative Commons by 360info™.